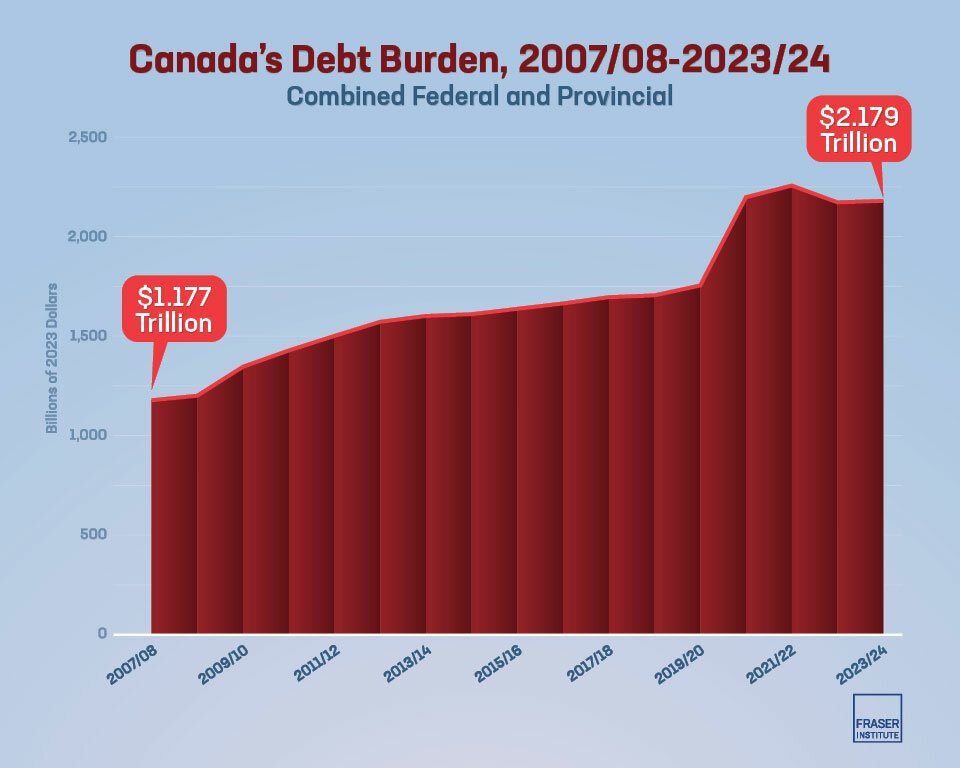

Canada’s combined federal and provincial debt has nearly doubled in the last 16 years, finds Fraser Institute, a non-partisan Canadian public policy think-tank, in a recent report, Growing Debt Burden for Canadians: 2024 Edition.

Credit: Fraser Institute

The debt has escalated from $1.18 trillion in 2007/08 to an estimated $2.18 trillion in the current year. This dramatic increase, according to Jake Fuss, the institute’s director of fiscal studies, poses significant fiscal challenges for both the federal and provincial governments.

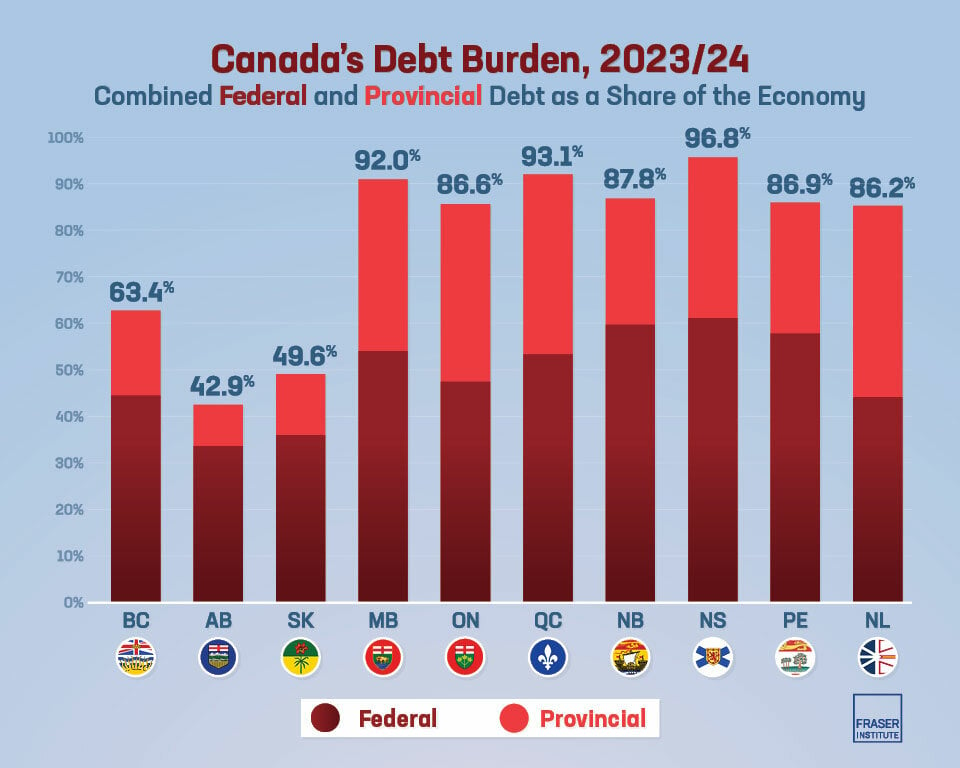

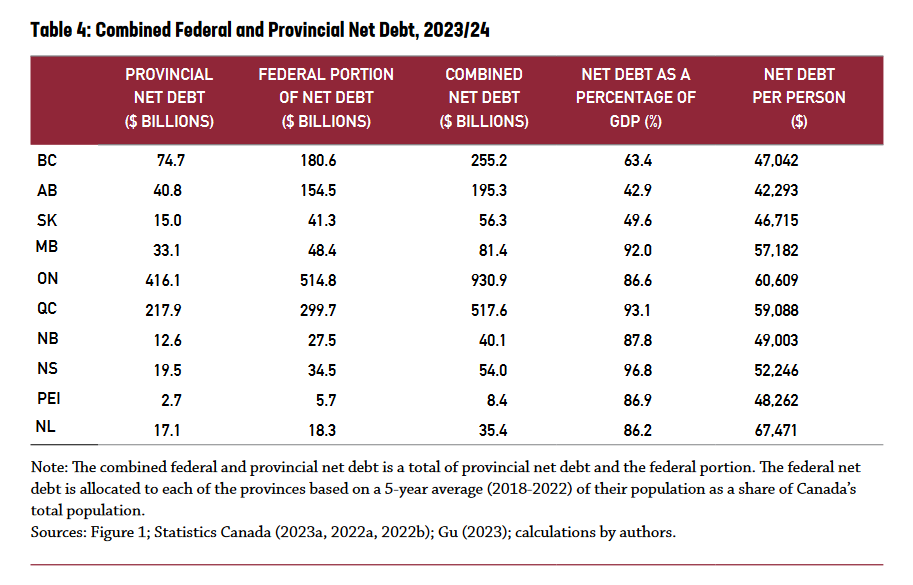

The study focuses on net debt, a key measure of government indebtedness that accounts for the total debt minus financial assets held by the governments. It indicates that the combined debt now constitutes 76.2% of Canada’s economy. This surge in debt includes substantial increases in various provinces, with Newfoundland and Labrador experiencing the highest debt-to-GDP ratio at 41.6% in 2023/24. Alberta, despite having the lowest debt-to-GDP ratio currently at 9.0%, witnessed a significant rise from a -13.4% ratio in 2007/08.

Credit: Fraser Institute

The Atlantic provinces, particularly Nova Scotia, have emerged as the region with the highest combined federal-provincial debt burden relative to their economies. Nova Scotia’s debt burden stands at 96.8% of its economy, the highest in Canada. Other Atlantic provinces like New Brunswick, Prince Edward Island, and Newfoundland and Labrador also feature high on this list.

Alberta’s recent budgetary surpluses have dramatically reduced its debt burden. From 2020/21 to 2023/24, Alberta’s provincial debt is projected to decrease by more than 40%, from $68.1 billion to $40.8 billion.

Per person, the combined debt varies considerably across provinces, with Newfoundland & Labrador topping the list at $67,471, followed by Ontario at $60,609 and Quebec at $24,877 per person. In contrast, Alberta has the lowest per-person debt at $8,832.

Fraser Institute says the total federal net debt per person has risen 52.6% since 2007/08 and is expected to reach $33,682 this year.

Credit: Fraser Institute

Growing government debt significantly hampers economic growth and private investment.

“It’s important for Canadians to understand the magnitude of the country’s combined government debt because deficits and debt today result in higher taxes in the future,”

said Fuss in a news release.

Interest payments are a significant burden resulting from government debt, akin to household obligations on mortgages or credit cards. As governments allocate more revenue to these payments, less funding becomes available for tax relief or essential programs like healthcare, education, and social services.

As government debt increases, long-term interest rates often rise, leading to higher borrowing costs in the private sector. This escalation in costs discourages private capital investment, subsequently affecting productivity and economic performance. Additionally, governments may raise taxes to service debt, further impeding growth.

Fraser Institute says the surge in government debt since 2007/08 necessitates strategic long-term planning by federal and provincial governments to address this issue, particularly post-COVID-19, as it diverts resources from vital programs and undermines economic competitiveness.

When you add in consumer debt and mortgages. It’s closer to 141,000.00 per capita nationally. We will have to either allow the raping and pillaging of our natural resources or our standard of living will decline dramatically. This does not leave our youth with any wiggle room and is incredibly irresponsible on the part of Canadian leadership…