The federal government introduced Tax-Free First Home Savings Account as part of the 2022 Budget, where Canadian residents can save up to $40,000 to buy their first home.

Today, the Department of Finance has released the draft legislative proposals of various measures including the Tax Free First Home Savings Account (FHSA) for public comment. FHSA is a “tax-free in, tax-free out” account where you can deduct contributions – up to $8,000 per year (the annual maximum) – from income, but the investment growth in the Tax-Free First Home Savings Account will not be taxable.

These are the details of the Tax Free First Home Savings Account released for public comment:

When will Tax Free First Home Savings Account (FHSA) start:

Ottawa says Canadians will be able to open and contribute to an FHSA sometime in 2023. Those who open an account in 2023 will be able to contribute the full $8,000 annual limit, irrespective of the time FHSA officially comes into existence.

Who can open and contribute to FHSA:

- An individual who is a resident of Canada and at least 18 years of age.

- An individual must be a first-time home buyer who has not owned a home in which they lived at any time during the part of the calendar year before the account is opened or at any time in the preceding four calendar years. Ownership includes beneficial ownership but excludes a right to acquire less than 10% of a qualifying home.

Unlike RRSP, the FHSA holder would be the only taxpayer permitted to claim deductions for contributions made to their FHSA. You would not be able to contribute to their spouse or common-law partner’s FHSA and claim a deduction.

Closing of an FHSA:

As per the news release, an FHSA would no longer be an FHSA account and an individual would not be permitted to open an FHSA, after December 31 the year in which the earliest of these events occurs:

- The fifteenth anniversary of the individual first opening an FHSA; or

- The individual turns 71 years old.

If there are any savings in the account that were not used to buy a home, they can be transferred on a tax-free basis into an RRSP or Registered Retirement Income Fund (RRIF). This can be done until December 31 of the year following the year of their first qualifying withdrawal. All other withdrawals will be taxable.

The transfer to RRSP or RRIF would not reduce the limit of those accounts.

How much can you contribute and how much is tax deductible:

The lifetime limit on contributions would be $40,000, with an annual contribution limit of $8,000. This means that a person can contribute lesser than $8000 in a calendar year. The remaining amount can be carried over to the next year. That is, if you only contributed $5000 in 2023 to FHSA, you can save $3000 plus $8000 in the year 2024.

You will be able to claim an income tax deduction for contributions made in a particular taxation year, but unlike RRSPs, contributions made within the first 60 days of a given calendar year could not be attributed to the previous tax year.

You would also be allowed to transfer funds from an RRSP to an FHSA on a tax-free basis, subject to the FHSA annual and lifetime contribution limits and the qualified investment rules.

A person can have multiple FHSA accounts, but the total amount contributed to all of their FHSAs should not exceed the annual and lifetime contribution limits.

Income, losses and gains in respect of investments held within an FHSA, as well as qualifying withdrawals, would not be included (or deducted) in computing income for tax purposes or taken into account in determining eligibility for income-tested benefits or credits like the Canada Child Benefit and the Goods and Services Tax Credit.

As per the news release, the Canada Revenue Agency (CRA) would provide basic FHSA information to support taxpayers in determining how much they can contribute in a given year.

You will be allowed to hold the same qualified investments that are currently allowed to be held in a TFSA including mutual funds, publicly traded securities, government and corporate bonds, and guaranteed investment certificates.

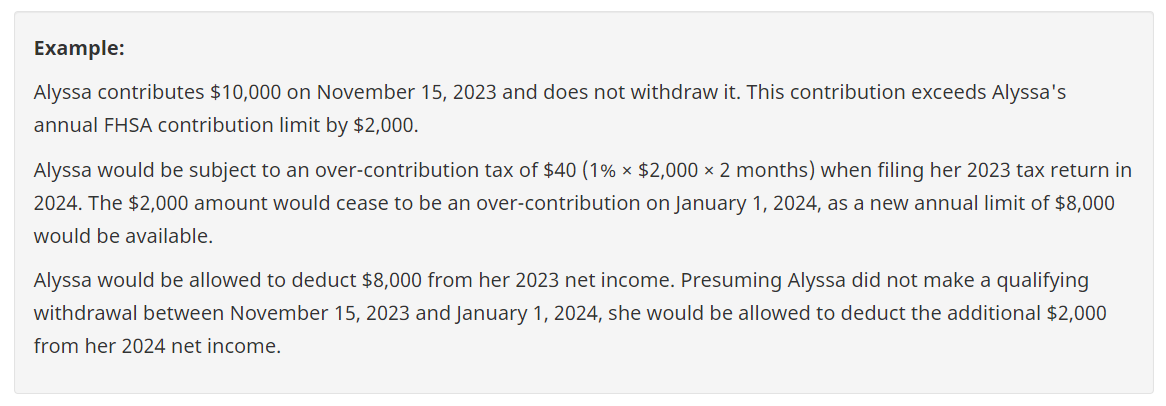

There will be a 1% tax on over-contributions to an FHSA and it would apply for each month (or a part of a month) to the highest amount of such excess that exists in that month. The rule is similar to TFSA.

Example of overcontribution as per the news release/Canada.ca

The annual contributtion taxpayer’s annual contribution limit is reset at the beginning of each calendar year. Hence over-contributions from a previous year may cease to be an over-contribution.

Contributions made to an FHSA following a qualifying withdrawal being made (i.e., when buying a first home) would not be deductible from net income.

What is a qualifying withdrawal:

A person can withdraw the entire amount of available FHSA funds on a tax-free basis in a single withdrawal or a series of withdrawals if they meet the following rules:

- The taxpayer must be a first-time home buyer at the time a withdrawal is made. That is the person should not have owned a home in which they lived at any time during the part of the calendar year before the withdrawal is made or at any time in the preceding four calendar years, but qualifying withdrawal is allowed within 30 days of moving into a new home.

- The taxpayer must also have a written agreement to buy or build a qualifying home before October 1 of the year following the year of withdrawal and intend to occupy the qualifying home as their principal place of residence within one year after buying or building it.

A qualifying home would be a housing unit located in Canada. A share in a co-operative housing corporation that entitles the taxpayer to possess, and have an equity interest in a housing unit located in Canada, would also qualify. However, a share that only provides a right to tenancy in the housing unit would not qualify.

All other withdrawals would be taxable at source and just like RRSP withdrawals, financial institutions are required to collect and remit withholding tax on non-qualifying withdrawals.

The detailed proposal of FHSA is available as Design of the Tax-Free First Home Savings Account.