2024 is the year when the Canada Pension Plan (CPP) enhancement’s final stage takes effect.

The Canada Pension Plan (CPP), a cornerstone of retirement income for Canadian workers, underwent significant enhancements in 2019. These changes aimed to bolster retirement income for Canadians, addressing the financial needs of those without workplace pension plans. The CPP, funded by contributions from workers, employers, and self-employed individuals, applies to nearly all Canadian workers outside Quebec, which operates the Quebec Pension Plan (QPP).

Participation in the CPP is mandatory for most individuals over 18 who work in Canada outside Quebec and earn above $3,500 annually. Those earning below this threshold are exempt from CPP contributions.

What CPP Enhancement Means:

A key feature of the enhanced CPP is the eventual 50% increase in the maximum retirement pension. That is, when today’s young worker (who works a full 40 years) retires in 2064, they will receive 50% more pension than those who retired recently.

With the enhancement, the income replacement level of CPP will increase from 25% to 33% of a worker’s pensionable earnings by 2064. This boost also extends to survivor and disability pensions.

The enhancement’s impact varies depending on an individual’s earnings and contribution duration. CPP Contributions are calculated based on annual earnings between the minimum and maximum limits, with the government annually setting the maximum, known as the Year’s Maximum Pensionable Earnings (YMPE).

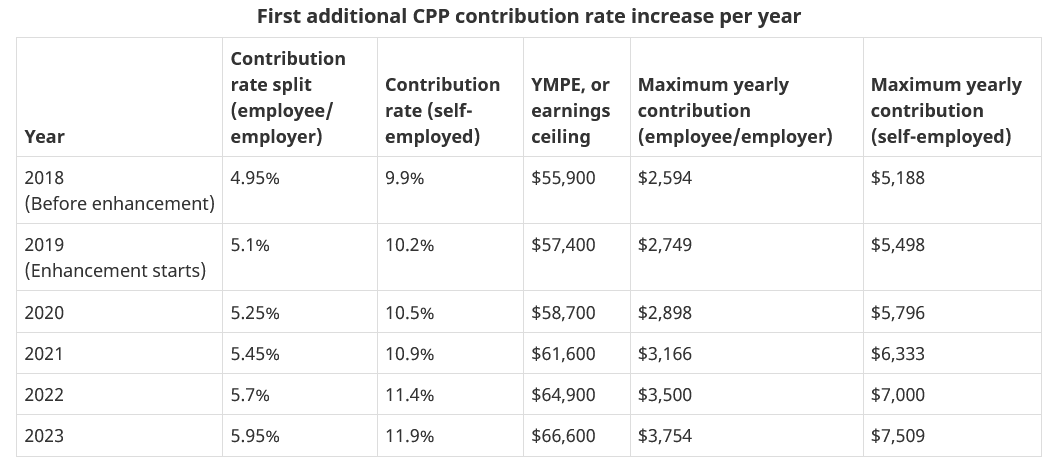

Since 2019, CPP contribution rates have been gradually increasing, affecting employees and employers to a 1% increase for employees and employers and a 2% increase for self-employed individuals by January 2023. For instance, an employee earning $55,000 in 2023 will contribute around $128.75 more than in 2022. The greatest benefit accrues to new workforce entrants, while those nearing retirement will see a smaller increase.

Credit: CRA/Canada.ca

What is new in 2024 – Year’s Additional Maximum Pensionable Earnings (YAMPE) and Second Additional CPP contributions (CPP2):

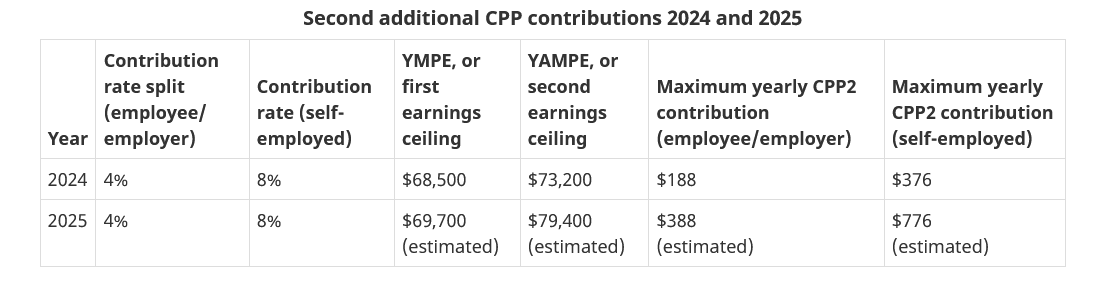

In 2024, a second earnings ceiling, the Year’s Additional Maximum Pensionable Earnings (YAMPE), will be introduced. This allows for additional contributions on income above the YMPE up to the YAMPE, forming part of the CPP enhancement.

This second ceiling, YAMPE, will be approximately 7% higher than YMPE in 2024. Employees and employers will contribute an additional 4% on earnings exceeding the YMPE up to the YAMPE, while self-employed individuals will contribute 8% on earnings within this range. The contribution rates are set to remain constant indefinitely after these adjustments.

As an employee, this means you will contribute additional money (CPP2 contributions) to your future pension, which is also tax deductible.

2024 CPP contribution rates and amounts:

The Canada Pension Plan (CPP) will have its maximum pensionable earnings increased to $68,500 from $66,600 in 2023, with the basic exemption amount remaining at $3,500.

The new second earnings ceiling of $73,200 is introduced for calculating second additional CPP contributions (CPP2), affecting earnings between $68,500 and $73,200.

Contribution rates for employees and employers stay at 5.95%, with maximum contributions rising to $3,867.50 each.

For self-employed individuals, the rate remains at 11.90%, with a maximum contribution of $7,735.00. CPP2 contributions are set at 4% for employees and employers (maximum $188.00 each) and 8.00% for self-employed individuals (maximum $376.00). Contributions will not be required beyond $73,200 in earnings.

New T4 boxes: If you have made additional CPP2 contributions, you will see entries in boxes 16A and 17A in the 2024 T4 slip (you get it before the end of February 2025).

How to Calculate Additional CPP Contributions for 2024:

If you make less than $68,500:

- As $68,500 is the 2024 maximum pensionable earnings limit, your annual CPP contribution will be (annual income-$3500)*0.0595.

- If you are self-employed, you also pay the employer portion. Hence your annual CPP contribution will be (annual income-$3500)*0.119

- CPP2 contribution will not apply.

If you make more than $68,500 but less than $73,200:

Your CPP will have two parts: Base CPP contribution and CPP2 contribution.

For 2024, an additional 4% contribution (called CPP2 contributions) will be mandatory and will be deducted above $68,500 (the first earnings ceiling, YMPE), up to $73,200 (second earnings ceiling, YAMPE). If you are self-employed, the percentage deduction is 8%.

- If you are an employee, this is how the total contribution is calculated :

-

- Base CPP contribution: ($68,500 – $3500)*0.0595= $3,867.50

- CPP2 contribution = (Your income – $68,500)*0.04. The maximum contribution is $188, if your income is $73,200 [0.04*(73,200-68,500)]

- Total annual CPP contribution: $3,867.50+ CPP2 contribution.

-

- If you are self-employed:

-

- Base CPP contribution: ($68,500 – $3500)*0.119= $7,735

- CPP2 contribution = (Your income – $68,500)*0.08. The maximum contribution is $376, if your income is $73,200 [0.08*(73,200-68,500)]

- Total annual CPP contribution: $7,735+ CPP2 contribution.

-

If you make more than $73,200:

As the YAMPE limit for 2024 is $73,200, no additional amount will be deducted from your salary. This means that your annual CPP contribution will be $4,055.50 if you are employed and $8,111, if you are self-employed.

2025 & Beyond:

Credit: CRA/Canada.ca

The CRA website states, “In 2025, the second earnings ceiling will be set at an amount that is approximately 14% higher than the first earnings ceiling. From 2026 on, the first and second earnings ceiling will increase incrementally each year, but the contribution rates will remain the same indefinitely.”

CRA announces the Year’s maximum pensionable earnings (YMPE) and the year’s additional maximum pensionable earnings (YAMPE) every November.

More Information:

- Canada Pension Plan Enhancement: Second CPP Contribution

- CPP contribution rates, maximums and exemptions