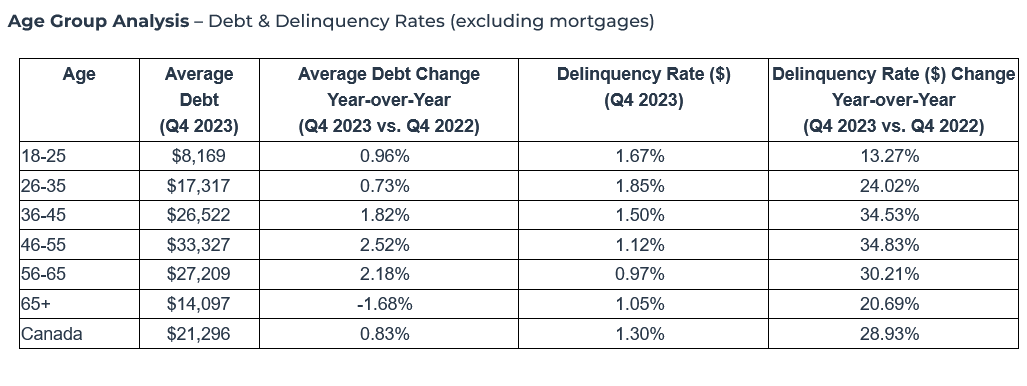

In another sign of financial strain faced by Canadians, Equifax Canada’s Market Pulse report for Q4 2023 reveals an upward trend in credit delinquencies.

Credit: Tierra Mallorca/ Unsplash

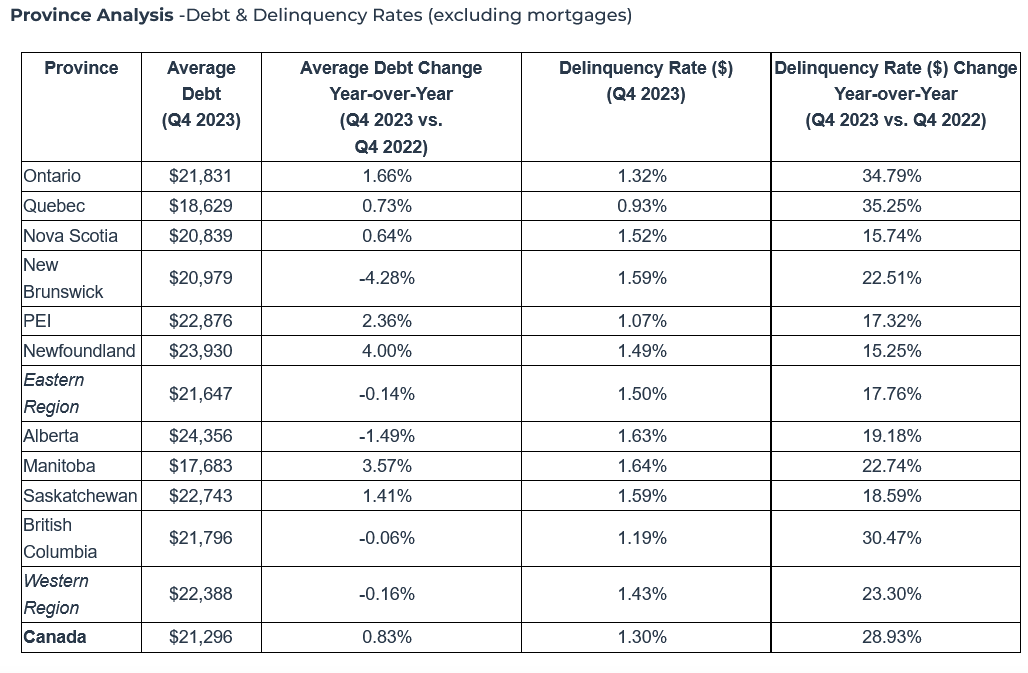

Non-mortgage delinquencies have risen by 28.9% since Q4 2022, reaching a 1.3% rate, while mortgage delinquencies have spiked by 52.3%, from 0.09% to 0.14%. Particularly hard-hit are Ontario and British Columbia, where mortgage delinquencies have increased by 135.2% and 62.2%, respectively.

The report finds that young homeowners in these regions are missing more payments, indicating heightened financial stress.

Credit: Equifax

The economic strain extends to mortgage renewals, with average monthly payments rising by $457 post-renewal, and even higher in Ontario and BC, where increases exceed $680. This has led to deteriorating credit performance among those facing steep hikes in mortgage payments.

Credit: Equifax

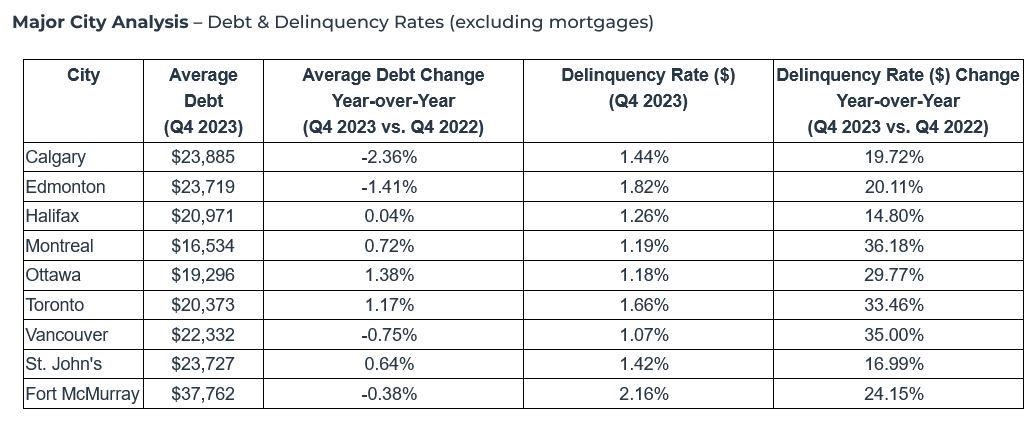

The Q4 2023 financial data reveals a mixed picture across major Canadian cities.

Calgary and Edmonton residents managed to lower their average debt by 2.36% and 1.41%, reaching $23,885 and $23,719, respectively. Yet, these reductions did not prevent delinquency rates from climbing, with Calgary experiencing a 19.72% year-over-year increase to 1.44%, and Edmonton seeing a 20.11% surge to 1.82%.

Equifax Canada

In contrast, Montreal reported a modest debt increase of 0.72% to $16,534, but it also faced the steepest delinquency rate hike of 36.18%, indicating a delinquency rate of 1.19%. Ottawa and Toronto saw their debts rise to $19,296 and $20,373 with increases of 1.38% and 1.17%, alongside delinquency rates escalating by 29.77% and 33.46%, respectively.

Fort McMurray, despite a slight debt decrease of 0.38% to $37,762, reported a considerable delinquency rate jump of 24.15% to 2.16%, the highest among the listed cities.

Halifax and St. John’s experienced increases in delinquency rates to 1.26% and 1.42%, respectively, with year-over-year changes of 14.80% and 16.99%. Vancouver noted a 0.75% decrease in average debt to $22,332 but still faced a delinquency rate increase of 35.00%.

Equifax says the total consumer debt has climbed to $2.45 trillion, a 3.2% year-over-year increase, driven largely by a $15.9 billion rise in credit card debt to $116.2 billion.

Despite the holiday spending, there’s been a noticeable decline in the full repayment of credit card balances, with fewer consumers managing to clear their debts each month. This is particularly evident among younger individuals and those with substantial HELOC balances.

The report also highlights a significant rise in auto sector demand and a worrying increase in non-mortgage delinquency rates, with over 153,000 additional consumers missing payments in 2023.

Bankruptcy filings also have gone up by 8% year-over-year, with a notable 23.2% increase in mortgage holders filing for bankruptcy, especially in Ontario and BC. These indicators reflect the broader impacts of high living costs, inflation, and financial pressures affecting Canadians across the country.