Credit: RBC Royal Bank

On March 16th, Canada’s six largest banks– Bank of Montreal, CIBC, National Bank of Canada, RBC Royal Bank, Scotiabank, and TD Bank – announced that they will be offering customers “flexible solutions” including mortgage deferrals to get them through economic uncertainties due to COVID-19.

If you want to know what exactly is offered as mortgage deferrals, this is what the Canadian Banking Association said:

- Customers should understand that this is not mortgage forgiveness.

- COVID-related mortgage deferral is available for an indefinite period and customers do not face a deadline for having to seek relief. They can approach their bank as the need arises.

- Mortgage deferral means that payments are skipped for a defined period of time, during which interest which would otherwise be part of the deferred payments is added to the outstanding balance of the mortgage.

- The added interest is incorporated into the monthly payment, either when payments resume at the end of the deferral period or upon renewal at the end of the mortgage’s term.

Examples From Scotiabank & RBC

Mortgage Deferrals From Scotiabank:

Information; Call: 1-800-4-SCOTIA

- Mortgage payment deferrals are available for customers experiencing hardship.

- A mortgage payment deferral means that you will not be required to make regular payments on your mortgage (principal, interest and property taxes, if applicable) for up to 6 months.

- During the time you defer your mortgage payments, interest will accrue to the outstanding balance of the mortgage. The amount is incorporated into the monthly payment when mortgage payments resume at the end of the deferral period.

- If your mortgage payment includes an amount for property taxes, Scotiabank will continue to pay these on your behalf and this amount may be added to your mortgage account balance at the end of the deferral period (or the property tax component of your mortgage payment may be adjusted to cover this amount). This means your payments will be slightly higher after the deferral period ends.

- You will pay more interest over the life of your mortgage, but a deferral will also help you with your short-term cash flow. If you have creditor insurance for your mortgage, you will continue to be charged for your Scotia Mortgage Protection insurance premiums in order to maintain your coverage.

The example provided on the website:

Credit: Scotiabank

The above example shows that with a 5% interest rate and a 6 month of deferred payments on a $100,000 mortgage will add an additional $35.32 per month to the monthly payments and that your total mortgage amount will increase by $2,484.98.

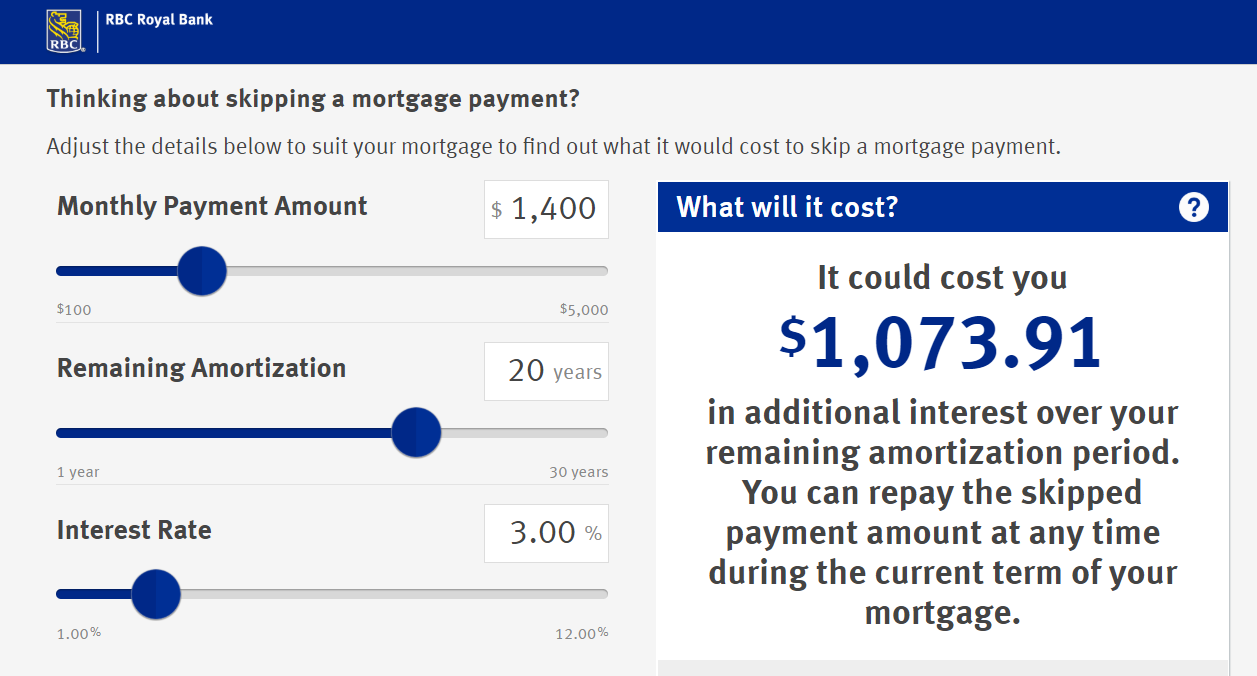

Mortgage Deferrals By RBC

RBC is asking clients to use online skip a payment due to high call volumes. According to RBC,

- There is no fee to skip a payment.

- When you skip a payment, the interest on the skipped payment is added to your outstanding balance and interest is charged on that amount. This means your mortgage balance will increase.

- Your payments won’t change during the term of your mortgage.

- Instead, at renewal, your monthly payment amount increases to account for the higher balance.

- When you skip a payment you must still pay the portion of your payment that covers your property taxes and HomeProtector Insurance Premium, if applicable.

- Using Skip-a-payment may significantly increase your interest costs over the life of your mortgage, so it’s important to carefully evaluate your financial situation and priorities before exercising this option.

- If you wish, you can repay your skipped payment anytime during the term of your mortgage. If you have made double-up payments during the term of your mortgage, you have the option to skip an equal amount of payments.

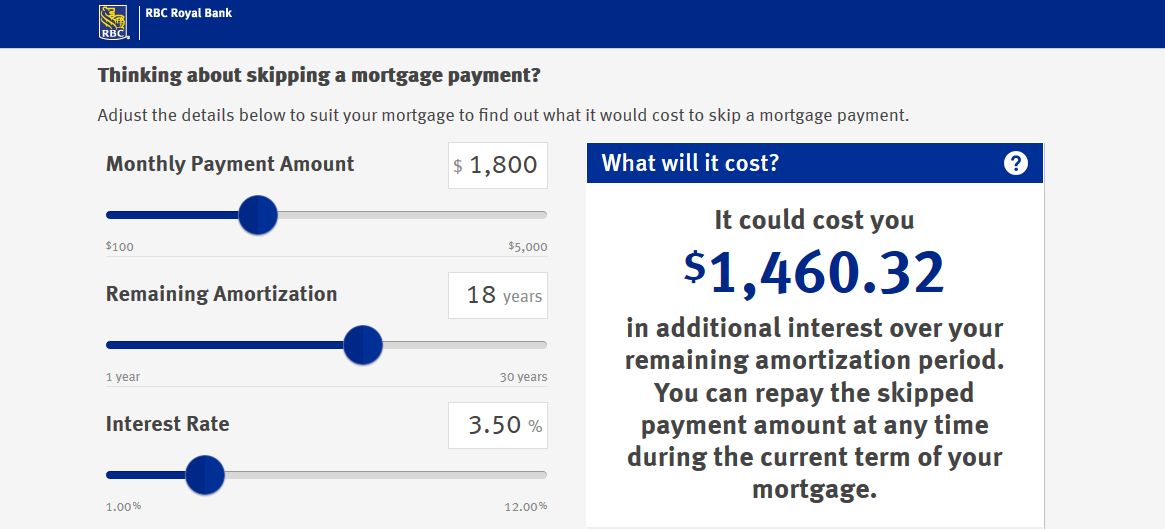

RBC Mortgage Deferral Calculator – Calculate Mortage Deferral Extra Interest Payment

Credit: RBC

RBC has a mortgage deferral calculator (Skip-A-Payment Mortgage Option) on its website that you can use to calculate your payments. Monthly mortgage payment of 1,800 and a 3.5% interest rate means that you will have to pay 1,460.32 over the 18 years of the remaining amortization period.